Taking a career break sounds like a simple math problem: save enough to cover your expenses, hand in your notice, done. But there are many other factors that need to be considered before you make the decision to take your career break.

Use the Planwell Career Break Planner to calculate your runway, stress-test your assumptions, and see how the break affects your full financial picture.

Try the career break planner →

There are many expenses to be considered when planning for a career break or sabbatical. Some expenses, such as health insurance costs, understandably go up during a break. But there are other expenses that may actually reduce.

What goes down:

What goes up (and catches people off guard):

Use the Planwell career break planner to get a month-by-month runway estimate that accounts for your specific expense profile.

Before you quit, decide — in writing, not just in your head — the maximum dollar amount you're willing to draw down from savings to fund your break. You do not want to empty your entire bank account or investments. This number should be specific: not "I'll use some of my savings" but "I will spend no more than $40,000, and my accounts will not drop below $X."

This matters because career breaks have a way of dragging on. A planned six months becomes nine. A medical expense appears. A job search takes longer than expected. Without a pre-committed ceiling, each individual spending decision feels reasonable in isolation but then you look up six months later to find you've gone further than you intended. It is important to make the decision once, clearly, before you're emotionally invested in staying on break.

No matter what, never dip into your retirement funds. Not only do you need to have money to cover retirement but you also need to pay a penalty if you withdraw early.

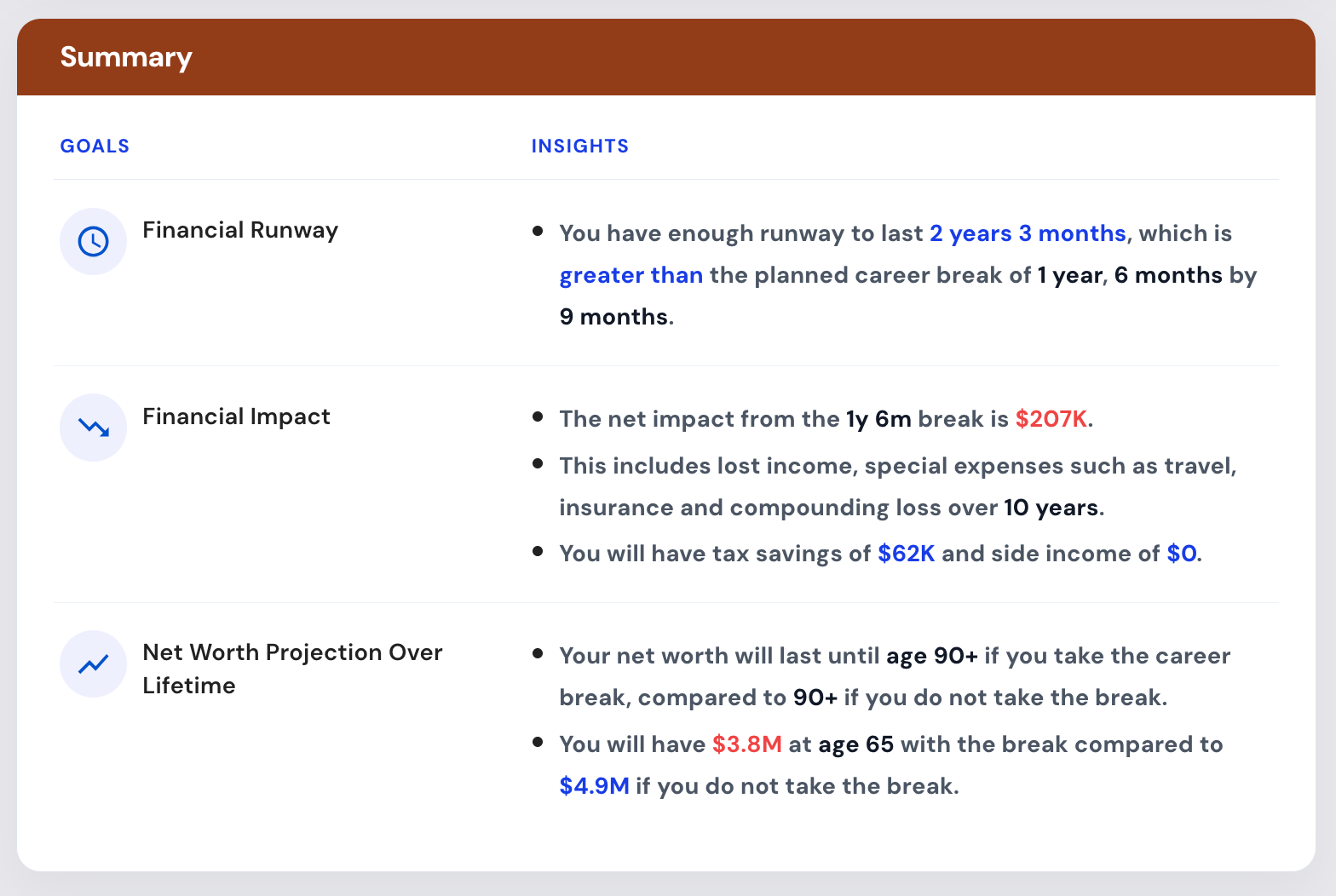

The full financial impact of break covers not just the lost salary but many other factors. You need to determine insurance costs, loss in compounding of savings, special expenses such as travel. On the other hand, you will also save some money in taxes (due to lower income levels).

Planwell’s career break planner tool accounts for all of these factors to tell you your true financial impact of taking a break.

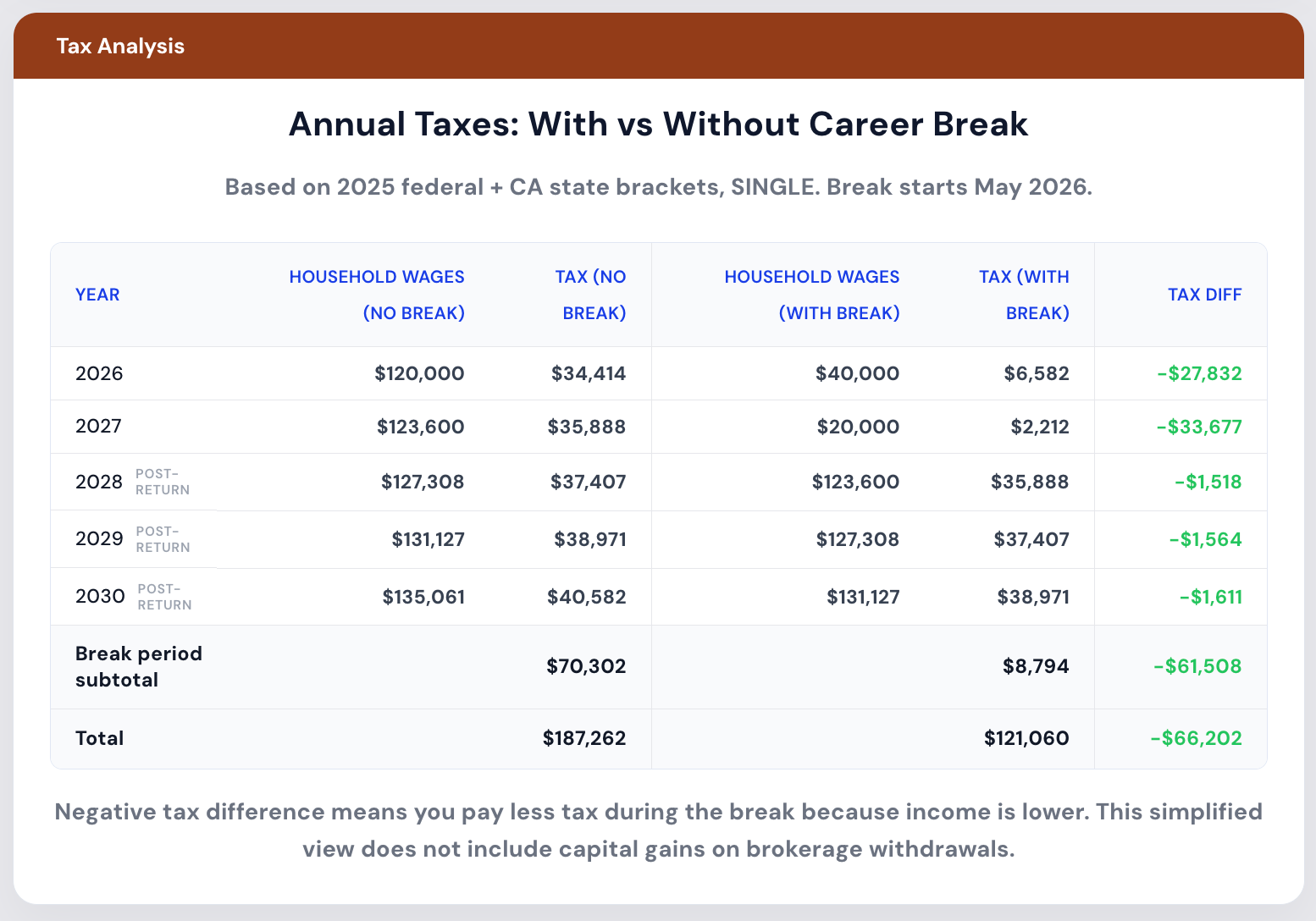

A career break will almost certainly drop you into a lower tax bracket. It is worth planning out your finances during the break keeping this as an important variable. Most people miss the tax optimization opportunities when they take a career break.

For example, if you earn $150,000 in a normal working year and your break-year income drops to $20,000 or zero, the difference in your effective federal tax rate can be substantial. That gap has practical implications that you can use strategically.

If your break-year income falls below the 0% long-term capital gains threshold (roughly $47,000 for single filers and $94,000 for married filing jointly in 2025), you may also be able to sell appreciated stocks or funds and owe nothing in federal capital gains taxes on the profit — as long as you held those assets for more than a year. For someone who has been sitting on gains in a taxable brokerage account, a low-income year is a rare opportunity to rebalance or harvest those gains at zero federal tax cost.

The mistake most people make is not modeling this in advance. Build your break-year tax picture before you quit, so you know what income you can take, sell, or convert without pushing yourself into a higher bracket. A low-income year is a rare and finite planning window; leaving it unexamined means leaving money on the table.

A career break is one of the best natural windows for Roth IRA conversions, and most people don't realize it until the window has already closed.

The mechanics are straightforward:

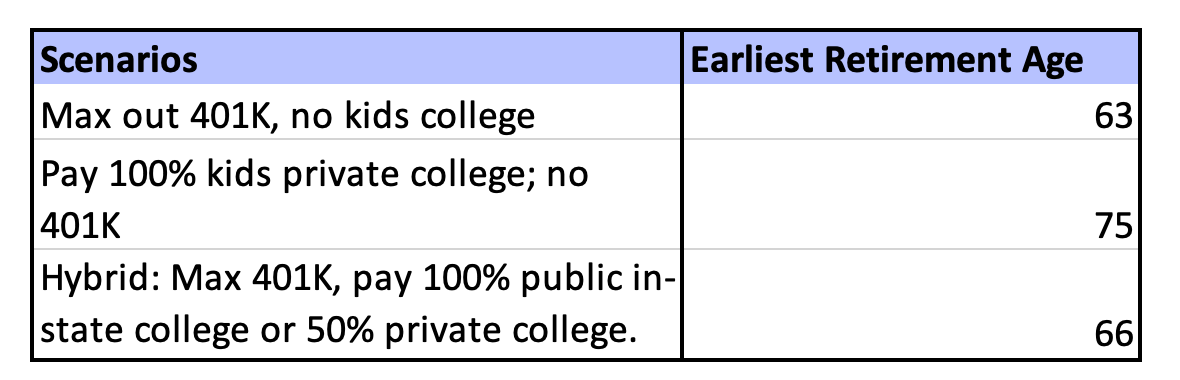

A six-month career break has greater implications than just impact to cash flow. It can affect other goals and so it is important to look at all your goals holistically when planning a break. Many people miss the impact to other goals, but this should be an important factor that influences your decision.

A career break can affect the following:

These goals are interdependent. A break that might be fine in isolation might delay your home purchase timeline by 18 months when you account for the full picture or reduce how much you are able to save for kids’ college.

Before you set a departure date:

Timing your re-entry is crucial but hard to precisely plan for. If your break ends during a hiring slowdown in your industry, the re-entry buffer (#2 above) becomes essential. Plan for the job search to take longer than you expect. The worst financial outcome from a career break isn't running out of money during the break — this can be planned for. But what is harder is returning to the job market underprepared and having to take a step down in comp to get back in.

Most financial planners recommend saving enough to cover 6–12 months of expenses before stepping away from a paycheck. But the right number depends on four variables:

Use a career break calculator to model your specific number rather than relying on a rule of thumb.

No. Your emergency fund should remain separate and intact throughout your break. It exists for genuine emergencies — a medical expense, an urgent home repair, an unexpectedly long job search — and not for planned living expenses. Depleting it to extend your break leaves you financially exposed at exactly the moment you can least afford it.

You have three main options:

There are a few risks for retirement savings that can be addressed with some careful planning:

If you work on a side gig or consulting or freelance work, you can open a Solo 401K or SEP IRA account.

Often yes. If your break-year income drops significantly, you may be in the lowest tax bracket of your adult life. Converting pre-tax retirement funds to a Roth IRA in that window lets you pay taxes on the conversion at a rate you may never see again during your working years. The key is calculating your conversion headroom carefully. Converting too much can push you into a higher bracket or trigger ACA subsidy clawbacks.

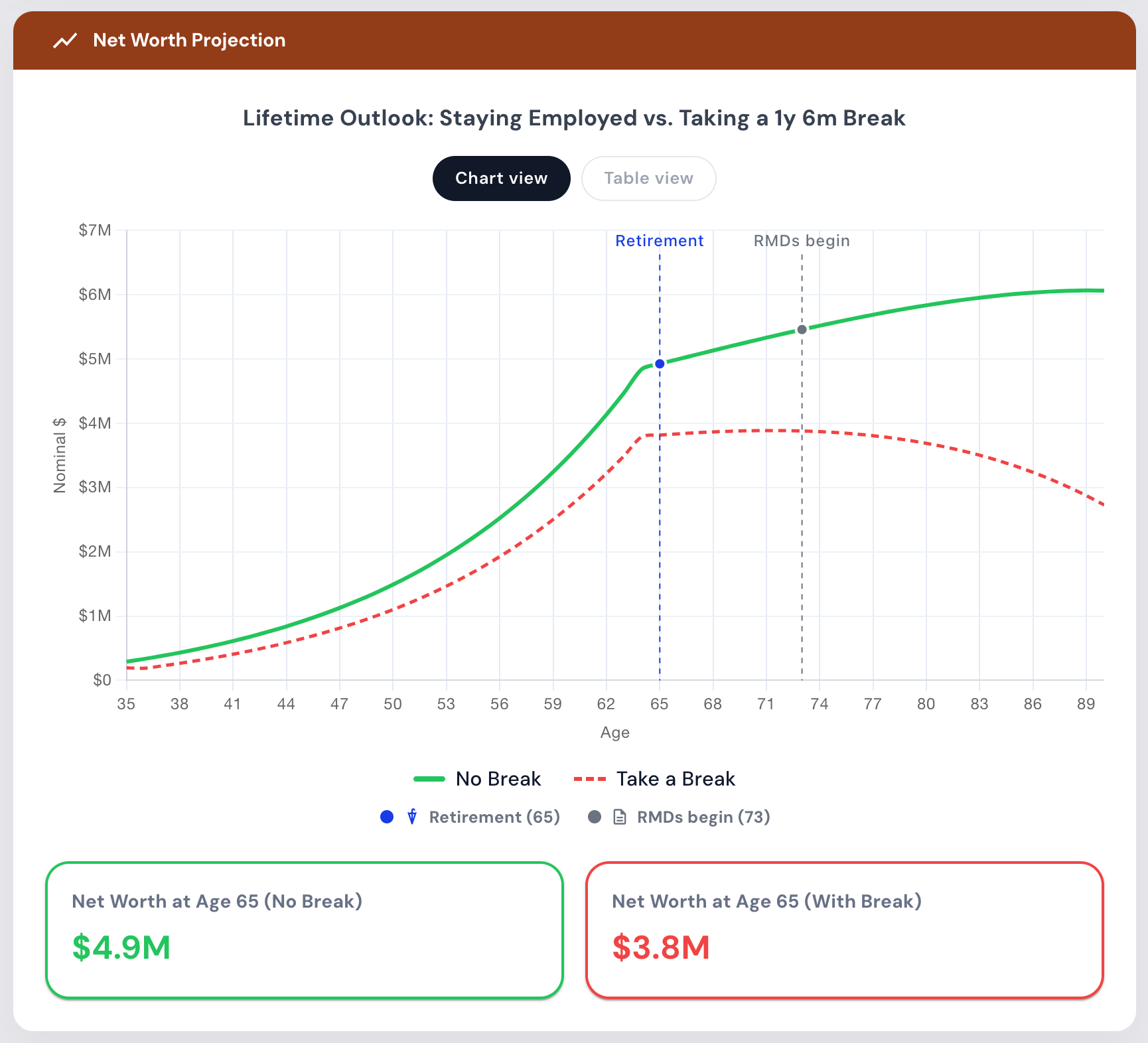

A career break affects more than just your break-year budget. It ripples into your home purchase timeline, college savings, and retirement date. A six-month break may feel financially contained, but reduced savings contributions during that period can shift a home purchase timeline by 12–18 months when you account for the full compounding effect. Model the break against all your goals together, not in isolation, before you commit.

Before you quit, decide the maximum dollar amount you're willing to draw from savings. Ringfence your emergency fund, down payment fund, and any earmarked retirement contributions first, then set your ceiling on what remains. A useful gut check: if drawing down to that ceiling would make you uncomfortable starting the next chapter of your career, you may have to try to cut expenses or the break needs more saving runway before it begins.

Timing matters more than most people realize.

Possibly not, depending on your income during the break. If you have no earned income and minimal investment income, you may fall below the threshold that triggers estimated tax requirements. However, if you do freelance or consulting work, receive significant dividends, or execute a Roth conversion during the break, you may owe estimated taxes. It's worth a one-time check with a CPA in the first year of your break to avoid an underpayment penalty.

At least 12–18 months before your target departure date. That window gives you time to build your break fund without stress, max out retirement contributions strategically, investigate health insurance options, and model the impact on your other financial goals. People who plan with less than six months of runway tend to either undershoot their savings target or rush decisions that have long-term consequences such as ACA enrollment or 401k rollovers.

Use Planwell's Career Break Planner to get a full financial analysis for your sabbatical or career break.