Design by Freepik

You've done the hard work - calculated your FIRE number, determined your target retirement age, and established your savings and withdrawal strategies. The path to financial independence and retiring early seemed clear.

Then the economic landscape shifted.

Market volatility, inflation concerns, and global economic uncertainty may have you questioning your carefully laid plans. In this climate, it is natural to be worried, but your FIRE journey does not need to be derailed.

Here is our step-by-step guide to ensure that you get back on track on your FIRE journey.

As a first step, start by crunching your numbers again with revised assumptions. You may want to consider higher inflation rates or lower rates of growth on your investments. Planwell’s AI financial planning tool can help you run the numbers and get instant results.

Here is an example to help you visualize the numbers.

Base case: Let’s say you are 38 years old making $250,000 gross income with a careful lifestyle of $8000 per month or $96,000 a year. You have saved up $150,000 in taxable savings and $200,000 in tax advantaged retirement savings.

Previously, you may have modeled Inflation at 2.5%; Income growth until retirement is 2%; Growth before and after retirement is 6% and 6% respectively.

Your earliest retirement age = 51

However, with the tougher economic conditions, you want to model higher inflation and lower growth rates on investments. So let us make inflation = 3.5% and rate of growth of investments = 5%.

Your revised age for retirement is 62.

Hmm, not what you were hoping for, exactly.

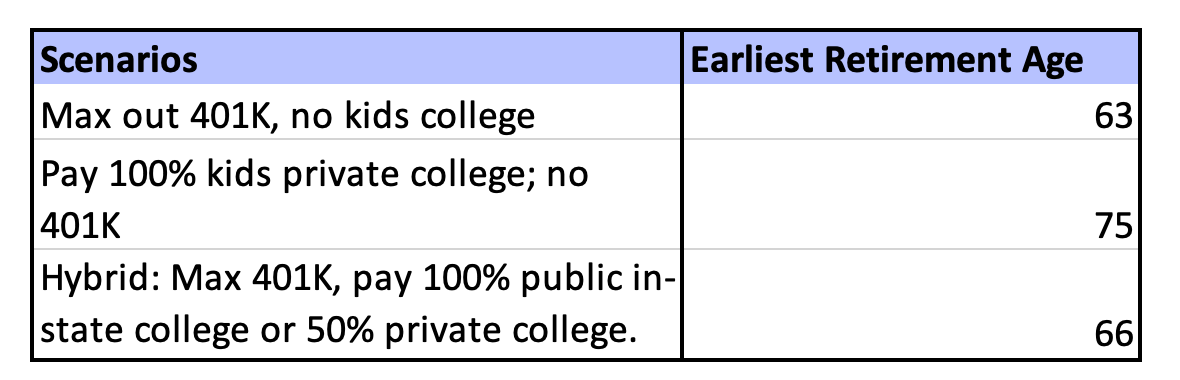

Now let us see what options you may have.

Revised FIRE calculations for a tough economy: Use the ‘what-if scenario’ planner to test a few alternative scenarios:

Now your FIRE age is 55, closer to your original goal.

Planwell’s ‘what-if’ feature can help you estimate the monthly expense levels you need in order to hit your FIRE goals. Once you have this expense number, go over your current expenses to find opportunities to cut costs. It is hard to cut fixed costs such as housing or utilities all of a sudden, but you can find opportunities to cut your variable and discretionary expenses such as shopping, dining or entertainment

If you really would like to prioritize FIRE, you can also think about whether you could adopt a Lean FIRE lifestyle and live on a lower income post-retirement. On the other hand, if you are willing to take on a low-stress part-time job, you may want to consider a Barista FIRE lifestyle.

Market downturns can pose risks to job security and many companies are announcing layoffs. It would be wise to beef up emergency funds to last you for a longer period. For example, if you have typically had 3 months’ emergency funds so far, try to save more until you have at least 6-12 months’ worth of funds in your emergency kitty.

It is natural to get into panic mode when your stocks, RSUs and retirement funds crash suddenly. But it is important to not do impulsive selling and certainly do not try to time the market. Historical data shows that stocks do bounce back after market drops. “According to Dimensional Investing, 3 year returns can be greater than 30% after a 10%-20% drop. But five years after market declines of 10%, 20%, and 30%, the average cumulative returns all top 50%.”

This means that holding stocks for the longer term, even if there is near term volatility, is usually beneficial and there is an opportunity to gain back a lot of the losses. This is where following the Boglehead investing approach can help you tide over market volatility in a systematic manner.

Market drops can be a good time to get a bargain on stocks. However, it is hard to time the market and predict when the stock market has hit a bottom. It is therefore important to stick with a disciplined long-term investment approach.

Dollar Cost Averaging (DCA) is a good strategy to derive the benefits of market drops while managing risks. With the DCA approach, you would buy the same amount worth of stocks every month so that you buy more stocks when the prices are low and you buy fewer stocks at higher prices when the market is high.

Investors can sell loss-making investments to offset or reduce capital gains taxes on investments that are sold at a profit. This is called tax loss harvesting. While it is not advisable to do panic-selling during a market downturn, it is a good idea to do tax loss harvesting on investments that are not profitable and unlikely to bounce back.

Economic uncertainty can be nerve wracking for FIRE enthusiasts but it remains achievable with thoughtful adjustments. To start with, re-evaluate your FIRE numbers and retirement timelines with more conservative assumptions such as higher inflation and lower investment returns.

Planwell’s financial planner can help you model these scenarios and figure out whether tradeoffs such as cutting expenses and lower withdrawal rates in retirement can help you get back on track. Tighten your budget by trimming discretionary expenses and consider lifestyle options like Lean or Barista FIRE. Increase your emergency funds to handle job insecurity in a turbulent economy.

When it comes to investing, staying the course is essential. Resist panic selling, and instead, stick with strategies like Dollar Cost Averaging and tax loss harvesting to navigate market volatility and capitalize on long-term growth. Ultimately, FIRE in a tough economy is about adaptability, resilience, and a disciplined approach to financial planning.

At Planwell, we are building a fully automated AI financial planner and advisor to help you make super personalized financial decisions such as how much house you can afford, while considering your lifestyle, retirement goals and other key factors.

We will be launching the product in the coming months. Stay tuned for an update. Join our waitlist for exclusive access to the free PlanWell beta. In the meantime, check out our blog posts to help you plan your finances.